Joe Biden’s $5.8T budget includes the largest tax increases in US history. But that doesn’t begin to describe just how terrible this is. Thirty-six tax hikes will cost taxpayers $2.5 trillion. It seriously harms the rich, investors, workers, ranch owners, inheritance, small businesses, stocks, savings, retirements, and that’s just the beginning. It will greatly damage the oil industry.

This is meant to turn us into socialists along with the rest of the nearly $6 trillion dollar budget.

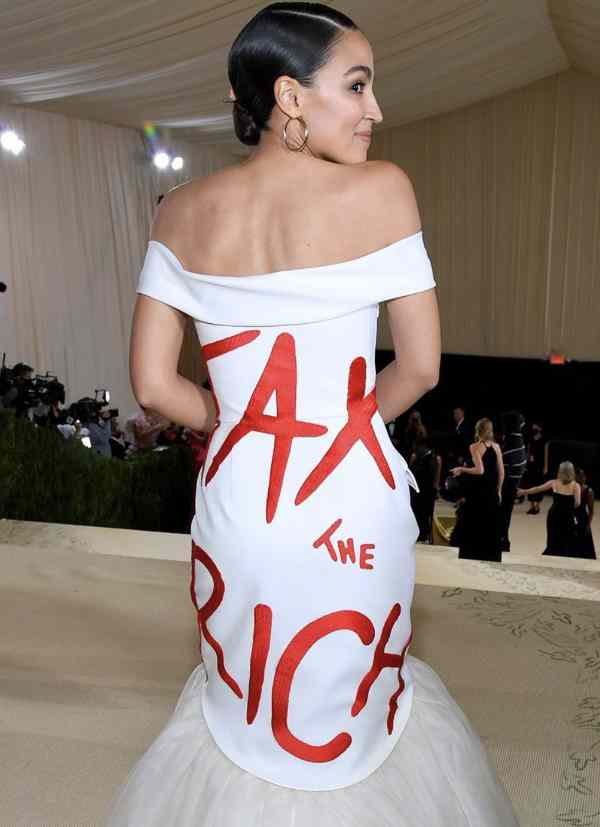

And they said it was only going to tax the rich.

The Americans for Tax Reform posted a summary and we are posting some of it but you can read the descriptions of the taxes on their website.

- Raise the corporate income tax rate to 28 percent: $1.3 trillion tax increase

After accounting for state corporate taxes, Biden will give the U.S. a 32 percent corporate rate, a tax rate significantly higher than Communist China’s 25 percent tax rate.

This tax increase will be passed along to families in the form of higher prices of goods and services.

Some economists say 70% of the taxes will hit workers.

A corporate tax increase will also threaten the life savings of families by reducing the value of publicly traded stocks in brokerage accounts or in 401(k)s.

- Increase the top income tax rate to 39.6 percent: $186.8 billion tax increase

This tax increase will hit small business that are organized as sole proprietorships, LLCs, partnerships and S-corporations. These “pass-through” entities pay taxes through the individual side of the tax code.

- Double the capital gains rate to 40.8 percent and the imposition of a second death tax by imposing capital gains taxes on unrealized assets at death: $174 billion tax increase

The U.S. currently has a combined capital gains rate of over 29 percent, inclusive of the 3.8 percent Obamacare tax and the 5.4 percent state average capital gains rate. Under Biden, this rate would approach 50 percent. This would give the U.S. a capital gains tax that is significantly higher than foreign competitors.

Under Biden’s plan, Californians will pay a top capital gains tax rate of 54.1 percent (37% + 3.8% + 13.3% California state rate = 54.1%).

The budget will also impose the 40 percent capital gains tax on the unrealized gains of every asset owned by a taxpayer when they die. This will be imposed in addition to the existing 40 percent Death Tax and will disproportionately fall on family-owned businesses, many of which are asset rich, but cash poor.

- Impose a 20 percent minimum tax on “billionaires”: $360.8 billion tax increase

This tax, called a “billionaire minimum income tax,” would impose an annual 20 percent tax on taxpayers with income and assets that exceeding $100 million, a $360 billion tax increase.

This tax is just the latest attempt by the Democrats to reshape the tax code and pass a tax on unrealized gains.

It would create a “mark to market” regime that would force Americans to pay taxes every year on the paper gain in the value of assets (i.e. stocks, collectibles, real estate). It would empower the IRS, encourage taxpayers to move assets overseas, and could grow to hit millions of Americans over time. It would also harm the economy, impose retroactive taxation, and has failed everywhere it has been tried before.

- Apply the Undertaxed Profits Rule: $239 billion tax increase

This would help enact the 15 percent global minimum tax effort.

-

Prevent basis shifting by related parties through partnerships: $61.7 billion tax increase

-

Tax carried interest capital gains as ordinary income: $6.6 billion tax increase

Raising taxes on carried interest capital gains could eliminate 4.9 million jobs and cause pension funds to lose $3 billion per year, according to a study by the U.S. Chamber of Commerce’s Center for Capital Markets Competitiveness.

The financial security these returns provide to American savers, including firefighters, teachers, and police officers, will be threatened if lawmakers raise taxes on carried interest capital gains.

- Repeal deferral of gain from like-kind exchanges: $19.6 billion tax increase

The budget proposes disallowing taxpayers from utilizing 1031s if they have gains exceeding $500,000. 1031s are not a tax loophole as some claim but are important tax provisions promoting reinvestment and liquidity.

Repealing this provision would harm smaller real estate investors by forcing them to forego new investments or go into debt to finance transactions.

- Repeal expensing of intangible drilling costs (IDCs): $10.7 billion tax increase

The expensing of IDCs allows companies to recover costs such as labor, site preparation, equipment rentals, and other expenditures for which there is no salvage value. IDCs often represent 60 to 80 percent of total production costs. This tax hike could result in the loss of over a quarter-million good-paying jobs by 2023.

- Repeal enhanced oil recovery credit: $1.56 billion tax increase

This provision would repeal the 15 percent credit for eligible costs attributable to enhanced oil recovery (EOR) projects like the costs of depreciable or amortizable tangible property or intangible drilling and development costs (IDCs). This credit is a bipartisan provision to incentivize carbon capture and sequestration, ultimately leading to less greenhouse gas emissions.

- Repeal credit for oil and natural gas produced from marginal wells: $1.9 billion tax increase

This repeals a credit for oil and natural gas produced from marginal wells, which is limited to 1,095 barrels of oil or barrel-of-oil equivalents per year.

-

Repeal exception to passive loss limitations provided to working interests in oil and natural gas properties: $83 million tax increase

-

Repeal percentage depletion with respect to oil and natural gas wells: $13 billion tax increase

Percentage Depletion allows taxpayers to deduct the cost of oil and gas wells as a statutory percentage of the gross income of such property. This provision is used by small, independent, and family-owned oil and gas companies, and royalty owners like farmers and ranchers.

- Increase geological and geophysical amortization period for independent producers: $10.2 billion tax increase

The amortization period for geological and geophysical expenditures incurred in connection with oil and natural gas exploration in the United States is two years for independent producers and seven years for integrated oil and natural gas producers.

-

Repeal expensing of exploration and development costs: $932 million tax increase

-

Repeal percentage depletion for hard mineral fossil fuels: $2.3 billion tax increase

Repeals a provision of the tax code that allows companies to deduct 10 percent of their sales revenue to reflect the declining value of their investment.

- Repeal capital gains tax treatment for royalties: $595 million tax increase

Royalties received on the disposition of coal or lignite currently qualify as a long-term capital gain. The budget repeals this, requiring this income to be taxed at the higher ordinary income rate.

- Repeal the exemption from the corporate income tax for fossil fuel publicly traded partnerships: $1 billion tax increase

Partnerships that derive at least 90 percent of their gross income from depletable natural resources, real estate, or commodities are exempt from the corporate income tax. Instead, they are taxed as partnerships. This proposal would repeal this provision for publicly traded fossil fuel partnerships, requiring them to be taxed as corporations.

- Repeal the Oil Spill Liability Trust Fund (OSTLF) excise tax exemption for crude oil derived from bitumen and kerogen-rich rock: $404 million tax increase

Because crude oil derived from bitumen and kerogen-rich rock are not treated as crude oil or petroleum products, it is exempt from the Oil Spill Liability Trust Fund tax of $0.09 per barrel of crude oil. This proposal would repeal this exemption.

- Eliminate the tax exemption for crude oil derived from bitumen and kerogen-rich rock from the superfund: $873 million tax increase

This proposal would extend the Superfund excise tax to other crudes such as those produced from bituminous deposits as well as kerogen- rich rock. It would also extend the Oil Spill Liability Trust Fund (OSLTF) tax to include these crudes as well. It would also eliminate the eligibility of the OSLTF for drawback.

- Eliminate drawback for the Oil Spill Liability Trust Fund: $698 million tax increase

- Conform definition of “control” with corporate affiliation test: $11.2 billion tax increase

This would modify the definition of “control” for purposes of Section 368(c) of the tax code to be at least 80 percent of total voting power and at least 80 percent of the total value of stock of a corporation.

- Eliminate tax deductions for expenses associated with relocating business operations overseas: $149 million tax increase

- Expand access to retroactive qualified electing fund elections: $39 million tax increase This would modify passive foreign investment company rules.

- Expand the definition of foreign business entity to include taxable units: $1.76 billion tax increase

- Repeal amortization of air pollution control facilities: $901 million tax increase

-

Modify income, estate, and gift rules for certain grantor trusts: $41.5 billion tax increase

Because so many family farms and businesses use Grantor Retained Annuity Trusts (GRATS) and other estate planning tools, this change would upend many of these taxpayers’ estate plans, forcing family businesses, farms, and ranches to hire expensive lawyers and accountants to rework their plans.

-

Require consistent valuation of promissory notes: $6.4 billion tax increase

-

Require 100 percent recapture of depreciation deductions as ordinary income for certain depreciable real property: $6.3 billion tax increase

-

Retroactively repeal the conservation easement deduction for partnerships: $18.6 billion tax increase

The government will change these laws after the fact.

- Limit use of donor-advised funds to avoid private foundation payout requirement: $64 million tax increase

- Extend the period for assessment of tax for certain Qualified Opportunity Fund investors: $95 million tax increase

-

Establish an untaxed income account regime for certain small insurance companies: $9.6 billion tax increase

-

Expand pro rata interest expense disallowance for business-owned life insurance: $6.8 billion tax increase

-

Correct “drafting errors” in the taxation of insurance companies under the Tax Cuts and Jobs Act of 2017: $787 million tax increase

-

Define the term “ultimate purchaser” for purposes of diesel fuel exportation: $139 million tax increase

Will the crony capitalists bail out on their Brandon?

I don’t feel sorry for them and they couldn’t get the trains to run on time if Harry Callahan put a S&W up to their heads.

Everyone has to take a haircut in muh democracy.

It is for the good of the collective after all and we are in this together.

Hurt everyone? Finally the precious indispensable glorious equality.

No shirking, comrades.

A new world will arise from sacrifice.

Emperor Schwab has spoken and his Pinocchio handlers in the WH will deliver.

Forward! Yes we can!

So Traitor Joe and the Democrats want to raise taxes when we have gone into stagflation. The Outcome will be a Depression and the Collapse of the Dollar and Banks. Even if you have financed a house at say 3%, it will be increase to 20% or more next year. The fact that you have a 30 year mortgage will be irreverent, the Government will let the Banks do what they want and bail them out with tax money and the Government Printing Press if needed. If you own property the Government will tax you out of your house. The Goal is for the Government and the Oligarchs to own everything. The Tax code should be one page, you pay 10% off the top on all income and no one in America pays more then 15% tax on all income, property, etc. America has been a Communist Nation with the Government redistributing Income since the 1920s. The Federal Government Budget should only be 4% of GDP.

Comments are closed.